Press release

16.09.2025

Liquid alternatives in the first half of 2025: A turnaround in fund inflows – interest has returned

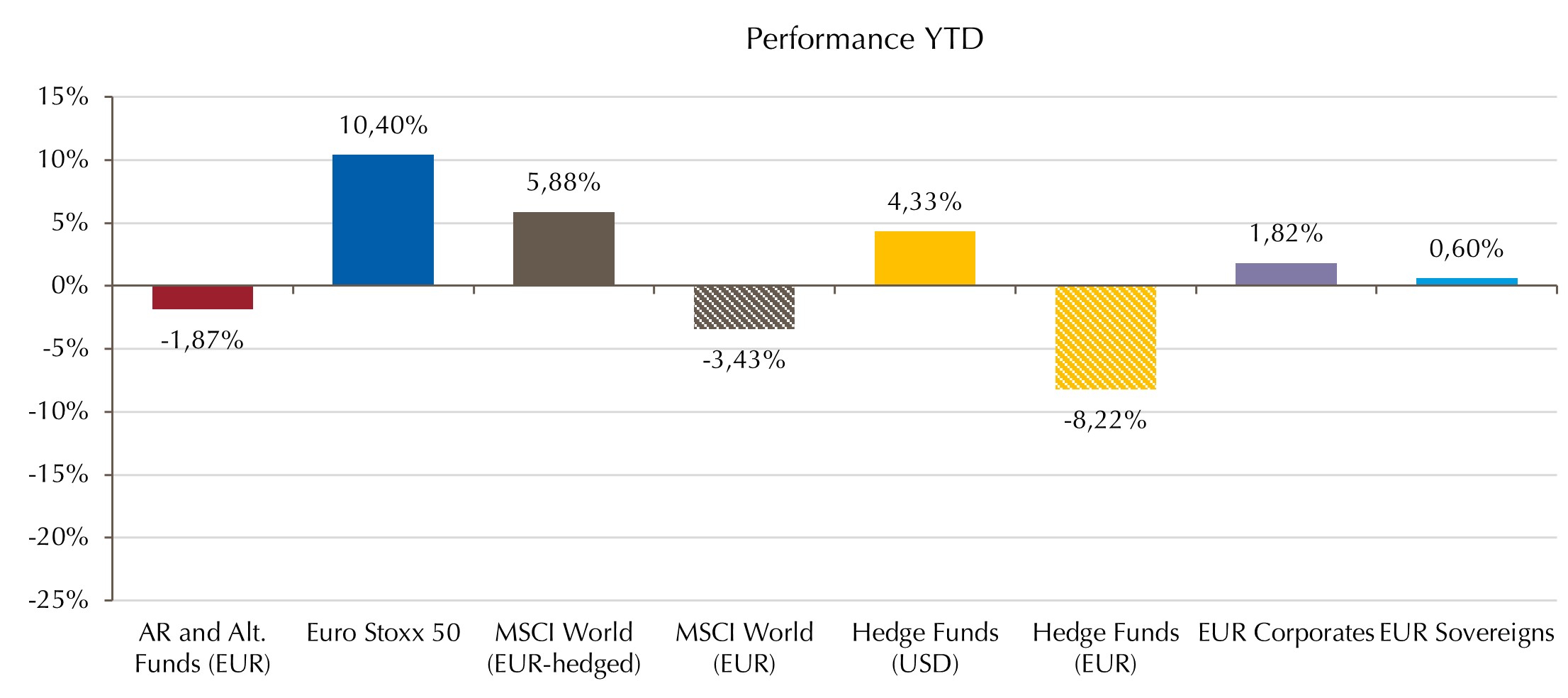

Liquid alternatives strategies recorded net inflows of €6.9 billion in all six months of the first half of 2025. This is a clear signal of renewed interest in this asset class and confirms the turnaround that began in the second half of 2024. The average return of eligible UCITS-compliant hedge funds in Germany was -1.87% from the perspective of a euro investor, mainly due to the historically strong depreciation of the US dollar of around 14% against the euro. This is the result of Lupus alpha’s semi-annual liquid alternatives study based on data from LSEG Lipper.

By far the most investor capital flowed into the asset class in the months of May and June – almost 70 per cent of net inflows in the first half of the year. This strong demand appears to have been triggered by US President Donald Trump’s announcement of new tariffs in April and the subsequent market turbulence. They acted as a catalyst for many investors to reassess their risk tolerance and led to a noticeable shift towards liquid alternative strategies – especially towards lower risk.

The largest inflows came from the two fixed income strategies: Absolute Return Bond and Alternative Credit Focus – a combined total of just under €4.9 billion. Defensive equity strategies such as Alternative Equity Market Neutral and Alternative Long/Short Equity also benefited from increased demand.

Institutional share classes accounted for just under half of the market volume in the first half of 2025 (49.5%) – only slightly below the record level at the end of 2024 (51.7%). Its high proportion underscores the confidence of institutional investors in the robust structures of liquid alternatives. Absolute return funds which were particularly low in risk were able to increase in this investor group (+EUR 0.8 billion).

The negative return on average of all funds of -1.87% in the first half of the year was mainly due to the weakness of the US dollar. This had a negative impact on globally oriented strategies with a high US share. Strategies with currency hedging or a focus on Europe thus clearly benefited European investors. Over a 5-year horizon, however, liquid alternatives continue to demonstrate their unchanged stabilising role in the portfolios of investors, achieving an average performance of just under 4.6% p.a. However, the strong dispersion of fund performance within the strategies requires investors to conduct careful due diligence when selecting funds.

Currency effect reduces liquid alternatives returns from a euro investor perspective

The strategies analysed were positively convincing in terms of risk behaviour: Despite the market upheaval in April, the maximum losses of many strategies remained moderate. The median for most strategies was below the MSCI World. In particular, the fixed income strategies Absolute Return Bond and Alternative Credit Focus impressed with defensive risk profiles. Strategies are also stable over a period of five years: eleven out of 14 categories recorded smaller drawdowns than global equities or euro bonds.

“Liquid alternatives have established themselves as an indispensable portfolio building block,” says Ralf Lochmüller, Managing Partner and CEO of Lupus alpha. “The data from the first half of the year clearly demonstrate the value of this asset class, especially for professional investors. With their specific risk/return profiles, liquid alternatives help investors better balance their portfolios.”

The downloadable white paper contains further detailed information, including a breakdown of the performance of individual strategies.

Download press release.

About the Lupus alpha “Liquid Alternatives” study: Since 2008, Lupus alpha has been evaluating the universe of absolute return and liquid alternatives funds on the basis of data from LSEG Lipper. The Study covers UCITS-compliant funds with an active management approach that are authorised for distribution in Germany. The Study focuses on market size, development and composition, performance in the investment segment and individual strategies, as well as key risk figures. It evaluates the three levels of aggregation – the overall universe, strategies within the universe, and funds within the strategies – a distinction is made between 14 strategies with a total of 715 funds.

About Lupus alpha: As an independent, owner-operated asset management company, Lupus alpha has been synonymous with innovative, specialised investment solutions for 25 years. As one of Germany’s European small and mid-cap pioneers, Lupus alpha is one of the leading providers of volatility strategies as well as collateralised loan obligations (CLOs). The specialist product range is rounded off by global convertible strategies and risk overlay solutions for institutional portfolios. The company manages approximately EUR 16 billion for institutional and wholesale investors, as well as EUR 6 billion in assets under overlay. For further information, visit www.lupusalpha.fr.

FURTHER INFORMATION